-----------------------------------------------------

Vienna Congress on Mathematical Finance (VCMF 2019)

Mon-Wed, September 9-11, 2019

VCMF Educational Workshop

Thu-Fri, September 12-13, 2019

https://fam.tuwien.ac.at/vcmf2019/

-----------------------------------------------------

*Deadline approaching:*

Standard registration ends on August 25, 2019

(from August 26, 2019, late registration fee applies):

https://fam.tuwien.ac.at/vcmf2019/registration.php

-----------------------------------------------------

The second Vienna Congress on Mathematical Finance (VCMF 2019) will be

held from September 9-11, 2019, once again at the new campus of WU

Vienna. The conference will bring together leading experts from various

fields of Mathematical Finance such as:

- Computational Methods and Machine Learning

- Credit Risk and Systemic Risk

- Limit Order Book and High Frequency Trading

- Markets with Frictions and Large Trader Models

- New Financial Markets (Cryptocurrencies,

Electricity, Energy, Securitization)

- Risk Measures and Optimization (Portfolio Optimisation,

Risk Allocation, Risk Aggregation)

- Robust Finance

- Stochastic and Rough Volatility

The conference program will feature plenary lectures, parallel sessions

with invited and contributed talks as well as poster sessions. Moreover,

there will be an attractive social program.

In the framework of a Panel Discussion (September 9, 2019) on the topic

"The big data revolution in mathematical finance" we offer the

conference participants a platform for discussions with a number of

renowned experts.

The conference is followed by a two-day Educational Workshop on

September 12 and 13, 2019, with lectures by internationally recognized

experts that will be a great learning opportunity in particular for

younger scientists.

The VCMF 2019 follows the successful previous edition, VCMF 2016, with

240 attendees, 83 talks and 28 poster presentations.

For further information including details on plenary and invited

speakers see the conference homepage at

https://fam.tuwien.ac.at/vcmf2019/

We are looking forward to meeting you in September in Vienna!

With kind regards from the VCMF 2019 organisers,

Mathias Beiglböck, Rüdiger Frey, Stefan Gerhold,

Friedrich Hubalek, Irene Klein, Thorsten Rheinländer,

Birgit Rudloff, Walter Schachermayer, Uwe Schmock

-----------------------------------------------------

Location:

Campus of WU Wien

Welthandelsplatz 1, 1020 Vienna/Wien, Austria

Organized by:

WU Vienna - Vienna University of Economics & Business

TU Wien - Vienna University of Technology

University of Vienna

Wolfgang Pauli Institute (WPI) Vienna

Gold Sponsor:

Raiffeisen Bank International (RBI)

BAWAG P.S.K.

Silver Sponsor:

B&W Deloitte

EnergieAllianz Austria (EAA)

EY

Meyerthole Siems Kohlruss

UNIQA Insurance Group

Plenary Speakers...

at the Congress:

- Beatrice Acciaio (London School of Economics)

- Fred Espen Benth (University of Oslo)

- Bruno Bouchard (Université Paris-Dauphine)

- Christa Cuchiero (WU Vienna)

- Paul Embrechts (ETH Zurich)

- Antoine Jacquier (Imperial College London)

- Sebastian Jaimungal (University of Toronto)

- Walter Schachermayer (University of Vienna)

at the Educational Workshop:

- Julien Guyon (Bloomberg, Columbia Univ., New York Univ.)

- Huyên Pham (University Paris VII Diderot)

- Josef Teichmann (ETH Zurich)

- Luitgard A. M. Veraart (London School of Economics)

Invited Speakers at the Congress:

- Emmanuel Bacry (École Polytechnique and Université Paris-Dauphine)

- Peter Bank (TU Berlin)

- Zachary Feinstein (Washington University in St. Louis)

- Damir Filipovic (EPFL and Swiss Finance Institute)

- Kathrin Glau (Queen Mary University of London)

- Archil Gulisashvili (Ohio University)

- Julien Guyon (Bloomberg, Columbia Univ., New York Univ.)

- Nikolaus Hautsch (University of Vienna)

- Blanka Horvath (King's College and Imperial College London)

- Ying Jiao (Université Claude Bernard Lyon 1)

- Sigrid Källblad (KTH Royal Institute of Technology)

- Eyal Neuman (Imperial College London)

- Marcel Nutz (Columbia University)

- Miklos Rasonyi (Alfred Renyi Institute of Mathematics)

- Nizar Touzi (École Polytechnique)

- Luitgard A. M. Veraart (London School of Economics)

https://fam.tuwien.ac.at/vcmf2019/speakers.php

Additionally on the first day of the congress there will be a panel

discussion with the title:

"The big data revolution in mathematical finance"

For further details see the program:

https://fam.tuwien.ac.at/vcmf2019/program.php

Registration:

Standard registration is possible until August 25, 2019.

From August 26, 2019, late registration fee applies.

https://fam.tuwien.ac.at/vcmf2019/registration.php

CPD:

The attendance at VCMF 2019 (full week, Sept. 9-13, 2019)

may qualify for up to 30 CPD credits for those delegates

whose national actuarial organization's CPD requirements

recognize VCMF 2019.

18 CPD credits for VCMF Congress (Sep 9-11) and

12 CPD credits for VCMF Educational Workshop (Sep 12-13).

VCMF 2019 is accredited by the AVÖ - Actuarial Assoc. of Austria.

For any requests, do not hesitate to write an e-mail to the conference &

workshop secretariat: vcmf2019(a)fam.tuwien.ac.at

---

"Le congrès danse beaucoup, mais il ne marche pas."

("The congress does not move forward, it dances.")

Prince Charles de Ligne’s famous words

at the Congress of Vienna (1814-1815)

-----------------------------------------------------

Sorry for the late announcement:

------------------------------------------------------------------------

IST Austria: Rough Paths

------------------------------------------------------------------------

Th./Fr., 04. & 05.07.2019, 10:15–11:45, Heinzel Seminar Room

IST Austria, Office Bldg West (I21.EG.101)

Peter Friz (TU Berlin, Germany)

http://page.math.tu-berlin.de/~friz/

Mini-course consisting of two sessions:

"Rough paths, Rough volatility and Regularity Structures"

Day #1 (https://talks-calendar.app.ist.ac.at/generate_invitation/2024):

The lecture is loosely based on the book [F-Hairer, Course on Rough

Paths, with an Introduction to Regularity Structures, Springer 2014] but

I will aim for a balance between introductory/standard material and

advanced topics taken from the 2nd edition (in preparation), hopefully

making the talk accessible to a diverse audience. Among the new material

I will introduce the rough volatility model from quantitative finance as

simple (but not too simple) example of a regularity structures that

exhibits many features also seen in the analysis of singular stochastic

partial differential equations like KPZ.

Day#2 (https://talks-calendar.app.ist.ac.at/generate_invitation/2025):

There will be some flexibility, and I am happy to cater to interests of

the audience. Possible topics include: Rough semimartingales, rough

paths with jumps, applications (of rough paths and regularitystructures)

to large deviations and Laplace method, applications to Multiscale

Systems, Homogenization.

With a printout of the invitations (see links above) you can use the

shuttle between Heiligenstadt and IST Austria for free.

(https://ist.ac.at/de/campus/anreise/)

------------------------------------------------------------------------

VCMF 2019 - Vienna Congress on Mathematical Finance...

------------------------------------------------------------------------

2nd Vienna Congress on Mathematical Finance 2019

& VCMF Educational Workshop

(jointly organised by WU Wien, TU Wien and University of Vienna)

WU Vienna, Mon-Fri, September 9-13, 2019

https://fam.tuwien.ac.at/vcmf2019/

*The early registration was prolonged until July 6, 2019.*

------------------------------------------------------------------------

To Whom it May Concern,

the TU Wien (FAM - Financial and Actuarial Mathematics), WU Vienna,

University of Vienna as well as the Wolfgang Pauli Institute jointly

organise the international event *VCMF 2019*:

Vienna Congress on Mathematical Finance

Mon-Wed, 9-11 September 2019

VCMF Educational Workshop

Thu-Fri, 12-13 September 2019

https://fam.tuwien.ac.at/vcmf2019/

*End of Early Registration:*

Reduced registration fee applies until 30 June 2019:

https://fam.tuwien.ac.at/vcmf2019/registration.php

*Abstracts:*

For the VCMF Educational Workshop all abstracts are online, for the VCMF

Conference the first abstracts are available. See:

https://fam.tuwien.ac.at/vcmf2019/program.php

*"START-Preis":*

Christa Cuchiero - plenary speaker of the VCMF Conferende as well as

(former) employee of TU Wien, University of Vienna and WU Vienna -

received the "START-Preis" of the Austrian Science Fund (FWF). This is

the highest Austrian award for young scientists of any discipline - the

recipients are selected by an international jury of experts. See:

https://fam.tuwien.ac.at/vcmf2019/news.php

*Vienna City Hall:*

The Conference Dinner takes place in the Vienna City Hall - same a the

Vienna Ball of Sciences or the worldwide renowned Life Ball. After the

delicious dinner participants can dance - true to the motto of the VCMF

event: "Mu and Sigma waltzing the Congress":

https://fam.tuwien.ac.at/vcmf2019/mu_sigma.php

With best regards,

Sandra

VCMF 2019 Conference & Workshop Secretariat

Katrin Artner and Sandra Trenovatz

+---------------------

|

| VCMF 2019 - Vienna, Austria

|

| Vienna Congress on Mathematical Finance

| Mon-Wed, September 9-11, 2019

|

| VCMF Educational Workshop

| Thu-Fri, September 12-13, 2019

|

| https://fam.tuwien.ac.at/vcmf2019/

|

+-------------------------------------------------

------------------------------------------------------------------------

Announcement of a Habilitation Talk at TU Wien

------------------------------------------------------------------------

Tu., 18.06.2019, 09:30, seminar room DA gelb 05a

TU Wien, 1040, Wiedner Hauptstr. 8, Freihaus, yellow area, 5th floor

Julia Eisenberg (TU Wien, Univ. Liverpool)

https://fam.tuwien.ac.at/~jeisenbe/

"A new approach for satisfactory pensions with no guarantees"

(Public Habilitation Talk / Habilitationskolloquium)

For further details (including abstracts) see

http://fam.tuwien.ac.at/contact/temp/Habilkolloquium_Eisenberg.pdf

------------------------------------------------------------------------

Universität Wien - Fachvortrag und Fallbeispiel aus der Beratungspraxis

------------------------------------------------------------------------

Tu., 18.06.2019, 17:30 c.t., Sky Lounge

Uni Wien, 1090 Vienna, Oskar-Morgenstern-Platz 1, 12th floor

Ferdinand Graf (d-fine)

"Künstliche Intelligenz in der Praxis"

David Haberfellner (d-fine)

"Kapitalmarkt und Ordermanagement"

(Mathematik in derUnternehmensberatung -

Fachvortrag und Fallbeispiel aus der Beratungspraxis)

Ausklang des Abends mit Snacks und Getränken.

For further details (including abstracts) see

http://fam.tuwien.ac.at/contact/temp/20190618_dfine.pdf

------------------------------------------------------------------------

Veranstaltungsreihe "Actuarial Modelling Club"

------------------------------------------------------------------------

Mo., 24.06.2019, 17:00, lecture hall 6

TU Wien, 1040, Wiedner Hauptstr. 8, Freihaus, 2nd floor, green area

Frank Schiller (Munich Re, DE)

"Moderne Life-Style Produkte in der Lebensversicherung

mit Big Data und Machine Learning"

(Actuarial Modelling Club)

For further details (including abstracts) and *registration* see

https://fam.tuwien.ac.at/vr/

------------------------------------------------------------------------

------------------------------------------------------------------------

Veranstaltungsreihe "Actuarial Modelling Club"

------------------------------------------------------------------------

We., 12.06.2019, 17:00, lecture hall 5

TU Wien, 1040, Wiedner Hauptstr. 8, Freihaus, 2nd floor, green area

Jan-Philip Gamp, Ehsan Ayatollahi (Milliman, DE)

"IFRS17 - unterschiedliche Bewertungsansätze

in der Lebensversicherung"

(Actuarial Modelling Club)

For further details (including abstracts) and *registration* see

https://fam.tuwien.ac.at/vr/

------------------------------------------------------------------------

Vienna Graduate School of Finance (VGSF)

------------------------------------------------------------------------

Th., 13.6.2019, 11:00-12:30, room D3.0.233

WU Wien, 1020, Welthandelsplatz 1, WU Campus, building D3, ground floor

Dimitri Vayanos (London School of Economics)

http://www.lse.ac.uk/Finance/People/Faculty/Vayanos

"Asset Management Contracts and Equilibrium Prices"

(Finance Research Seminar)

For further details (including abstracts) see

http://www.vgsf.ac.at/events/finance-research-seminar/

To find the room on the WU Campus search for "D3.0.233" on:

http://gis.wu.ac.at/?roomShow=D3.0.233

------------------------------------------------------------------------

Announcement of a Habilitation Talk at TU Wien

------------------------------------------------------------------------

Tu., 18.06.2019, 09:30, seminar room DA gelb 05a

TU Wien, 1040, Wiedner Hauptstr. 8, Freihaus, yellow area, 5th floor

Julia Eisenberg (TU Wien, Univ. Liverpool)

https://fam.tuwien.ac.at/~jeisenbe/

"A new approach for satisfactory pensions with no guarantees"

(Public Habilitation Talk / Habilitationskolloquium)

For further details (including abstracts) see

http://fam.tuwien.ac.at/contact/temp/Habilkolloquium_Eisenberg.pdf

------------------------------------------------------------------------

------------------------------------------------------------------------

Workshop 2 of the Thematic Program "Optimal Transport"

------------------------------------------------------------------------

Mo.-Fr, 03.- 07.05.2109, Boltzmann Lecture Hall, 2nd floor

Uni Wien / ESI, 1090 Wien, Boltzmanngasse 9/2

Workshop 2: Optimal Transport in Analysis and Probability

For further details (including abstracts) see

https://www.esi.ac.at/activities/events/2019/optimal-transport

- - - - - - - - - - - - - - -

To mention one of the talks:

- - - - - - - - - - - - - - -

Mo., 03.05.2109, 15:00-15:45:

Sigrid Källblad (KTH Stockholm)

"Stochastic control of measure-valued martingales

with applications to robust finance"

------------------------------------------------------------------------

Vienna Graduate School of Finance (VGSF)

------------------------------------------------------------------------

Fr., 07.06.2019, 11:00, room D3.0.225

WU Wien, 1020, Welthandelsplatz 1, WU Campus, building D3, ground floor

Robert Korajczyk (Northwestern University)

https://www.kellogg.northwestern.edu/faculty/directory/korajczyk_robert.aspx

"Arbitrage Portfolios"

(Finance Research Seminar)

For further details (including abstracts) see

http://www.vgsf.ac.at/events/finance-research-seminar/

To find the room on the WU Campus search for "D3.0.225" on:

http://gis.wu.ac.at/?roomShow=D3.0.225

------------------------------------------------------------------------

Veranstaltungsreihe "Actuarial Modelling Club"

------------------------------------------------------------------------

We., 12.06.2019, 17:00, lecture hall 5

TU Wien, 1040, Wiedner Hauptstr. 8, Freihaus, 2nd floor, green area

Jan-Philip Gamp, Ehsan Ayatollahi (Milliman, DE)

"IFRS17 - unterschiedliche Bewertungsansätze

in der Lebensversicherung"

(Actuarial Modelling Club)

For further details (including abstracts) and *registration* see

https://fam.tuwien.ac.at/vr/

------------------------------------------------------------------------

Veranstaltungsreihe "Actuarial Modelling Club"

------------------------------------------------------------------------

Tu., 24.06.2019, 17:00, lecture hall 6

TU Wien, 1040, Wiedner Hauptstr. 8, Freihaus, 2nd floor, green area

Frank Schiller (Munich Re, DE)

"Moderne Life-Style Produkte in der Lebensversicherung

mit Big Data und Machine Learning"

(Actuarial Modelling Club)

For further details (including abstracts) and *registration* see

https://fam.tuwien.ac.at/vr/

------------------------------------------------------------------------

------------------------------------------------------------------------

Announcement of Public PhD Thesis Defense at University of Vienna

------------------------------------------------------------------------

Friday, 17.05.2019, Besprechungszimmer / meeting room 9th floor

Uni Wien, 1090 Wien, Oskar-Morgenstern-Platz 1

12:30:

Annemarie Grass (Univ. Vienna)

"Multimarginal Solutions to the Skorokhod Embedding Problem

and the Information Paradox in Robust Mathematical Finance"

(Public PhD Thesis Defense)

13:00:

Manuel Eder (Univ. Vienna)

"A synthetic view on stochastic processes"

(Public PhD Thesis Defense)

------------------------------------------------------------------------

VCMF 2019 - Submissions possible until Saturday, May 18, 2019

------------------------------------------------------------------------

Vienna Congress on Mathematical Finance

& VCMF Educational Workshop

Vienna, September 9-13, 2019

https://fam.tuwien.ac.at/vcmf2019/

The submission deadline for contributed talks & posters

is Saturday, May 18, 2019.

https://fam.tuwien.ac.at/vcmf2019/registration.php

------------------------------------------------------------------------

WU Wien, Institute for Statistics and Mathematics

------------------------------------------------------------------------

Fr., 24.05.2019, 09:00, seminar room D4.4.008

WU Wien, 1020, Welthandelsplatz 1, WU Campus, building D4, 4th floor

Katia Colaneri (University of Leeds, UK)

https://physicalsciences.leeds.ac.uk/staff/1491/dr-katia-colaneri

"A class of recursive optimal stopping problems

with an application to stock trading"

(Research seminar - Statistics and Mathematics)

For further details (including abstracts) see

https://www.wu.ac.at/en/statmath/research/resseminar/

To find the room on the WU Campus search for "D4.4.008" on:

http://gis.wu.ac.at/?roomShow=D4.4.008

------------------------------------------------------------------------

------------------------------------------------------------------------

WU Wien, Institute for Finance, Banking and Insurance

------------------------------------------------------------------------

Mo., 13.5.2019, 12:00, room D4.0.019

WU Wien, 1020, Welthandelsplatz 1, WU Campus, building D4, ground floor

Steven Baker (University of Virginia)

https://www.commerce.virginia.edu/faculty/baker

"Asset Prices and Portfolios with Externalities"

(Finance Brown Bag Seminar)

For further details (including abstracts) see

https://www.wu.ac.at/en/finance/research/brown-bag-seminar/

To find the room on the WU Campus search for "D4.0.019" on:

http://gis.wu.ac.at/?roomShow=D4.0.019

------------------------------------------------------------------------

------------------------------------------------------------------------

WU Wien, Institute for Finance, Banking and Insurance

------------------------------------------------------------------------

We., 08.05.2019, 11:00, room D4.4.008

WU Wien, 1020, Welthandelsplatz 1, WU Campus, building D4, ground floor

Leopold Sögner (IHS)

https://www.ihs.ac.at/de/personen/leopold-soegner/

"Optimal High-Risk Investment"

(Finance Brown Bag Seminar)

For further details (including abstracts) see

https://www.wu.ac.at/en/finance/research/brown-bag-seminar/

To find the room on the WU Campus search for "D4.4.008" on:

http://gis.wu.ac.at/?roomShow=D4.4.008

------------------------------------------------------------------------

VCMF 2019 - Extended Submission Deadline

------------------------------------------------------------------------

2nd Vienna Congress on Mathematical Finance 2019

& VCMF Educational Workshop

(jointly organised by WU Wien, TU Wien, University of Vienna and WPI)

WU Vienna, Mon-Fri, September 9-13, 2019

https://fam.tuwien.ac.at/vcmf2019/

***UPDATE:***

The submission deadline for contributed talks & posters

is extended until Saturday, May 18, 2019.

https://fam.tuwien.ac.at/vcmf2019/registration.php

------------------------------------------------------------------------

------------------------------------------------------------------------

Joint Seminar: TU Wien, University of Vienna and WU Vienna

------------------------------------------------------------------------

Th., 18.04.2019, 15:45, Boltzmann Lecture Hall, 2nd floor

Uni Wien / ESI, 1090 Wien, Boltzmanngasse 9/2

Josef Teichmann (ETH Zurich, CH)

https://people.math.ethz.ch/~jteichma/

"Machine Learning in Finance"

(Vienna Seminar in Mathematical Finance and Probability)

Please note that time & place is different as usual!

For further details (including abstracts) see

https://fam.tuwien.ac.at/vs-mfp/

This talk is also part of the thematic program "Optimal Transport" - see

below.

------------------------------------------------------------------------

Thematic Program "Optimal Transport"

------------------------------------------------------------------------

Th., 18.04.2019, 13:45-16:45, Boltzmann Lecture Hall, 2nd floor

Uni Wien / ESI, 1090 Wien, Boltzmanngasse 9/2

Eric Carlen (Rutgers Univ.)

"Brascamp Lieb inequalities for fermions

and non-commutative mass transport"

Yvain Bruned (Univ. of Edinburgh)

"Geometric Stochastic Heat Equations"

Josef Teichmann (ETH Zürich)

"Machine Learning in Finance"

Th., 25.04.2019, 15:45-16:45, Boltzmann Lecture Hall, 2nd floor

Uni Wien / ESI, 1090 Wien, Boltzmanngasse 9/2

Mathieu Lewin (CNRS & Univ. Paris-Dauphine)

"Optimal Transport and Density Functional Theory"

May 6-10: Introductory School on Optimal Transport

May 13-17: Workshop 1: Optimal Transport: from Geometry to Numerics

June 3-7: Workshop 2: Optimal Transport in Analysis and Probability

For further details (including abstracts) see

https://www.esi.ac.at/activities/events/2019/optimal-transport

------------------------------------------------------------------------

------------------------------------------------------------------------

WU Wien, Institute for Statistics and Mathematics

------------------------------------------------------------------------

Fr., 12.4.2019, 09:00, seminar room D4.4.008

WU Wien, 1020, Welthandelsplatz 1, WU Campus, building D4, 4th floor

Michaela Szölgyenyi (University of Klagenfurt)

https://www.aau.at/en/statistics/team/szoelgyenyi-michaela/

"Convergence order of Euler-type schemes for SDEs

in dependence of the Sobolev regularity of the drift"

(Research seminar - Statistics and Mathematics)

For further details (including abstracts) see

https://www.wu.ac.at/en/statmath/research/resseminar/

To find the room on the WU Campus search for "D4.4.008" on:

http://gis.wu.ac.at/?roomShow=D4.4.008

------------------------------------------------------------------------

------------------------------------------------------------------------

Joint Seminar: TU Wien, University of Vienna and WU Vienna

------------------------------------------------------------------------

Th., 4.4.2019, 16:15(!), seminar room DC rot 07

TU Wien, 1040, Wiedner Hauptstr. 8, Freihaus, 7th floor, red area

Hanna Wutte (ETH Zurich)

https://www.math.ethz.ch/the-department/people.html?u=hwutte

"Randomized shallow neural networks

and their use in understanding gradient descent"

(Vienna Seminar in Mathematical Finance and Probability)

For further details (including abstracts) see

https://fam.tuwien.ac.at/vs-mfp/

------------------------------------------------------------------------

WU Wien, Institute for Statistics and Mathematics

------------------------------------------------------------------------

Fr., 5.4.2019, 09:00, seminar room D4.4.008

WU Wien, 1020, Welthandelsplatz 1, WU Campus, building D4, 4th floor

Nadja Klein (School of Business and Economics, HU Berlin)

http://www.wiwi.hu-berlin.de/de/professuren/vwl/statistik/members/personalp…

"Implicit Copulas from Bayesian Regularized Regression Smoothers"

(Research seminar - Statistics and Mathematics)

For further details (including abstracts) see

https://www.wu.ac.at/en/statmath/research/resseminar/

To find the room on the WU Campus search for "D4.4.008" on:

http://gis.wu.ac.at/?roomShow=D4.4.008

------------------------------------------------------------------------

Vienna City Marathon

------------------------------------------------------------------------

Sunday, 7.4.2019, 9:xx - 13:yy, 42.195 km through Vienna,

at the relay category this is: 15.5 + 6.0 + 9.3 + 11.395 km.

FAM starts with 4 relay teams:

FAM@TU speed measure

FAM@TU random walk

FAM@TU expected shortfall

FAM@TU no free lunch

You are welcome to cheer for us :-)

For further details - especially the results afterwards - see

https://www.vienna-marathon.com/

------------------------------------------------------------------------

-----------------------------------------------------

VCMF 2019 - Vienna, Austria

Vienna Congress on Mathematical Finance

Mon-Wed, September 9-11, 2019

VCMF Educational Workshop

Thu-Fri, September 12-13, 2019

https://fam.tuwien.ac.at/vcmf2019/

-----------------------------------------------------

To Whom it May Concern,

The second Vienna Congress on Mathematical Finance (VCMF 2019) will be

held from September 9-11, 2019, once again at the new campus of WU

Vienna. The conference will bring together leading experts from various

fields of Mathematical Finance such as:

- Computational Methods and Machine Learning

- Credit Risk and Systemic Risk

- Limit Order Book and High Frequency Trading

- Markets with Frictions and Large Trader Models

- New Financial Markets (Cryptocurrencies,

Electricity, Energy, Securitization)

- Risk Measures and Optimization (Portfolio Optimisation,

Risk Allocation, Risk Aggregation)

- Robust Finance

- Stochastic and Rough Volatility

The conference program will feature plenary lectures, parallel sessions

with invited and contributed talks as well as poster sessions. Moreover,

there will be an attractive social program.

The conference is followed by a two-day Educational Workshop on

September 12 and 13, 2019, with lectures by internationally recognized

experts that will be a great learning opportunity in particular for

younger scientists.

The VCMF 2019 follows the successful previous edition, VCMF 2016, with

240 attendees, 83 talks and 28 poster presentations.

For further information including details on plenary and invited

speakers invited see the conference homepage at

https://fam.tuwien.ac.at/vcmf2019/

Submission and Registration is open:

https://fam.tuwien.ac.at/vcmf2019/registration.php

We are looking forward to meeting you in September in Vienna!

With kind regards from the VCMF 2019 organisers,

Mathias Beiglböck, Rüdiger Frey, Stefan Gerhold,

Friedrich Hubalek, Irene Klein, Thorsten Rheinländer,

Birgit Rudloff, Walter Schachermayer, Uwe Schmock

-----------------------------------------------------

Location:

Campus of WU Wien

Welthandelsplatz 1, 1020 Vienna/Wien, Austria

Organized by:

WU Vienna - Vienna University of Economics & Business

TU Wien - Vienna University of Technology

University of Vienna

Gold Sponsor:

Raiffeisen Bank International

(further sponsors are welcome)

Plenary Speakers...

at the Congress:

- Beatrice Acciaio (London School of Economics)

- Fred Espen Benth (University of Oslo)

- Christa Cuchiero (WU Vienna)

- Paul Embrechts (ETH Zurich)

- Antoine Jacquier (Imperial College London)

- Sebastian Jaimungal (University of Toronto)

- Johannes Muhle-Karbe (Imperial College London)

at the Educational Workshop:

- Julien Guyon (Bloomberg, Columbia Univ., New York Univ.)

- Huyên Pham (University Paris VII Diderot)

- Josef Teichmann (ETH Zurich)

- Luitgard A. M. Veraart (London School of Economics)

Invited Speakers at the Congress:

- Emmanuel Bacry (Ecole Polytechnique and Université Paris-Dauphine)

- Damir Filipovic (L'Ecole Polytechnique Fédérale de Lausanne)

- Kathrin Glau (Queen Mary University of London)

- Archil Gulisashvili (Ohio University)

- Julien Guyon (Bloomberg, Columbia Univ., New York Univ.)

- Nikolaus Hautsch (University of Vienna)

- Blanka Horvath (King's College and Imperial College London)

- Ying Jiao (Université Claude Bernard Lyon 1)

- Sigrid Källblad (KTH Royal Institute of Technology)

- Marcel Nutz (Columbia University)

- Luitgard A. M. Veraart (London School of Economics)

- further speakers t.b.a.

https://fam.tuwien.ac.at/vcmf2019/speakers.php

Additionally on the first day of the congress there will be a panel

discussion with the title:

"The big data revolution in mathematical finance"

Panellists:

- Nikolaus Hautsch

Professor of Finance and Statistics

of University of Vienna

- Jonas Hirz

BELTIOS GmbH (Austria) and

Head of the Data Science Section of

the Actuarial Association of Austria (AVÖ)

- further Panellists t.b.a.

Moderator:

- Josef Teichmann

Full Professor of Financial Mathematics, ETH Zürich

For further details see the program:

https://fam.tuwien.ac.at/vcmf2019/program.php

Important dates and deadlines:

Submission:

The call for contributed talks & posters

is open until April 30, 2019.

Acceptance/rejection letters will be sent

end of May 2019 (June 7, 2019 at the latest).

Registration:

Early registration is possible until June 30, 2019.

Registration is possible until August 15, 2019.

Submission and Registration:

https://fam.tuwien.ac.at/vcmf2019/registration.php

CPD:

The attendance at VCMF 2019 (full week, Sept. 9-13, 2019)

may qualify for up to 30 CPD credits for those delegates

whose national actuarial organization's CPD requirements

recognize VCMF 2019.

18 CPD credits for VCMF Congress (Sep 9-11) and

12 CPD credits for VCMF Educational Workshop (Sep 12-13).

VCMF 2019 is accredited by the AVÖ - Actuarial Association of Austria.

For any requests, do not hesitate to write an e-mail to the conference &

workshop secretariat: vcmf2019(a)fam.tuwien.ac.at

---

"Le congrès danse beaucoup, mais il ne marche pas."

("The congress does not move forward, it dances.")

Prince Charles de Ligne’s famous words at the Congress of Vienna (1814-1815)

-----------------------------------------------------

To Whom it May Concern,

additionally to a talk this week we announce a few events of research

and cooperation partners as well as the "Vienna Congress on Mathematical

Finance (VCMF 2019)" co-organised by FAM @ TU Wien.

Best wishes, Sandra (Trenovatz)

------------------------------------------------------------------------

Veranstaltungsreihe "Actuarial Modelling Club"

------------------------------------------------------------------------

Th., 21.3.2019, 17:00, Freihaus Hörsaal 5

TU Wien, 1040, Wiedner Hauptstraße 8-10 , 2. Stock, grüner Bereich

Dr. Gerold Petritsch (EVN)

"Über den aktuariellen Tellerrand hinaus:

Data Science als Erfolgsfaktor in der Energiewirtschaft"

(Actuarial Modelling Club)

For further details (including abstracts) and registration see

https://fam.tuwien.ac.at/vr/

------------------------------------------------------------------------

------------------------------------------------------------------------

MathFinance - Frankfurt, April 2019

------------------------------------------------------------------------

MathFinance Conference

Frankfurt, April 8-9, 2019

MathFinance hosts the annual Conference in Frankfurt which is tailored

to the European finance community. Providing cutting-edge research and

brand new practical applications, the conference is intended for

practitioners in the areas of trading, quantitative or derivative

research, risk and asset management, insurance as well as for academics

studying or researching in the field of financial mathematics.

https://www.mathfinance.com/events/mathfinance-conference/

------------------------------------------------------------------------

Optimal Transport - Vienna, May/June 2019

------------------------------------------------------------------------

Thematic Programme "Optimal Transport"

The program brings together researchers working on Optimal Transport in

diverse areas, such as stochastic analysis, mathematical finance,

analysis in singular spaces, geometric inequalities, gradient flows,

optimal random matching, optimal transport for density matrices,

numerical methods, computer vision, and machine learning. The aim of the

proposed ESI programme is to establish interactions, encourage new

collaborations, and identify synergies between these different disciplines.

May 6-10: Introductory School on Optimal Transport

May 13-17: Workshop 1: Optimal Transport: from Geometry to Numerics

June 3-7: Workshop 2: Opt. Transport in Analysis and Probability

http://pub.ist.ac.at/~jmaas/ESI_OT2019/

------------------------------------------------------------------------

AMaMeF - Paris, June 2019

------------------------------------------------------------------------

9th General AMaMeF Conference

Paris, June 11-14, 2019 in Paris

AMaMeF, acronym for Advanced Mathematical Methods in Finance, is a

European network of research promoting the exchange and diffusion of

knowledge in the field of Mathematical Finance. Under the auspices of

AMaMeF numerous conferences, workshops and other scientific activities

have been organized. Among these the General AMaMeF Conferences have

been the biggest, and they are currently organized in a roughly

two-yearly schedule.

https://9amamef.sciencesconf.org

------------------------------------------------------------------------

VCMF 2019 - Vienna, September 2019

------------------------------------------------------------------------

2nd Vienna Congress on Mathematical Finance 2019

& VCMF Educational Workshop

WU Vienna, Mon-Fri, September 9-13, 2019,

jointly organised by WU Wien, TU Wien and University of Vienna

Submission of abstracts as well as registration is already possible:

https://fam.tuwien.ac.at/vcmf2019/

The VCMF 2019 follows the successful previous edition, VCMF 2016, with

240 attendees, 83 talks and 28 poster presentations.

------------------------------------------------------------------------

--------------------------------------------------------------------

Announcement of Public PhD Thesis Defense at TU Wien

--------------------------------------------------------------------

We., 13.3.2019, 14:00, conference room of the Deanery,

TU Wien, 1040, Wiedner Hauptstr. 8, Freihaus, green area, 9th floor

(8th floor, then staircase in the green area)

Christiane Elgert (FAM @ TU Wien)

"Theory of Distribution-Constrained Optimization Problems"

(Public PhD Thesis Defense)

For further details (including abstracts) see

https://fam.tuwien.ac.at/events/

--------------------------------------------------------------------

------------------------------------------------------------------------

PDE Afternoon at TU Wien

------------------------------------------------------------------------

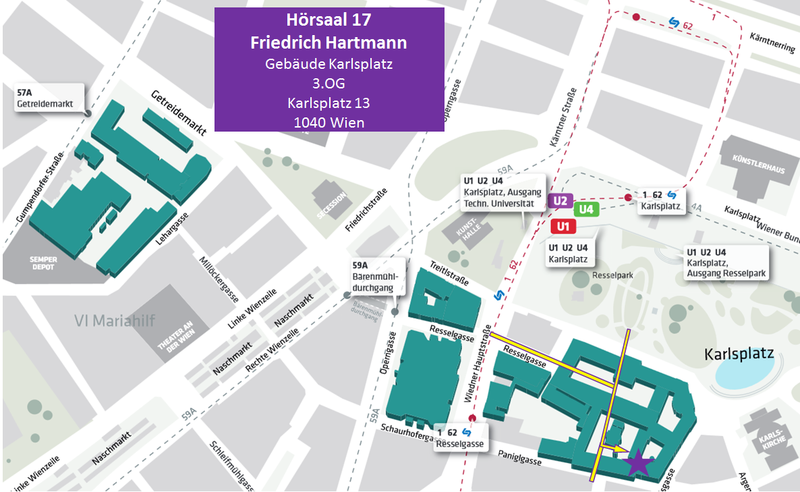

We., 06.03.2019, 15:30 bis 16:00, HS 17 Friedrich,

TU Wien, 1040, Karlsplatz 13, main building, staircase VII, 3rd floor

Gudmund Pammer (TU Wien)

"Stability of the weak transport / continuity

of super-hedging in finance"

(PDE Afternoon)

For further details see

https://www.univie.ac.at/sfb65/#!/public/events/details/?type=1&id=380

------------------------------------------------------------------------

TU ForMath — Forum Mathematik

------------------------------------------------------------------------

Th., 7.3.2019, 18:00 - 19:00, Freihaus Hörsaal 3

TU Wien, 1040, Wiedner Hauptstr. 8, Freihaus, 2nd floor, yellow area

Johannes Morgenbesser (Österreichische Nationalbank)

"Mathematics undercover: Die Mathematik hinter Blockchain und Bitcoin"

For further information see:

https://www.tuformath.at/vortraege/

------------------------------------------------------------------------

------------------------------------------------------------------------

Talks at University of Vienna

------------------------------------------------------------------------

Tu., 19.02.2019, 16:30, lecture hall HS13

Uni Wien, 1090 Wien, Oskar-Morgenstern-Platz 1, 2nd floor

Nicolas Juillet (Université de Strasbourg)

"Excursions and Transport"

Abstract:

Transport on the real line for power of the distance $d^p$ cost is

well-known especially when p>1 where the canonical quantile transport is

the unique optimal transport. For p=1 it is not unique and for p<1 it is

not optimal anymore and there is no uniqueness anymore. However, I will

present a natural transport problem providing a solution that catches in

a canonical way the transport behavior for p<1.

(https://mathematik.univie.ac.at/newsevents/nachrichtenvolldarstellung/news/…)

------------------------------------------------------------------------

------------------------------------------------------------------------

Joint Seminar: TU Wien, University of Vienna and WU Vienna

------------------------------------------------------------------------

Th., 24.01.2019, 16:30, lecture hall HS13

Uni Wien, 1090 Wien, Oskar-Morgenstern-Platz 1, 2nd floor

Nathael Gozlan (Université Paris 5 - René Descartes)

https://sites.google.com/view/nathaelgozlanmath

"Optimal transport for barycentric transport costs"

(Vienna Seminar in Mathematical Finance and Probability)

For further details (including abstracts) see

https://fam.tuwien.ac.at/vs-mfp/

------------------------------------------------------------------------

To whom it may concern,

I appologize for the second mailing this week, but I forgot to send out

the public PhD theses defense of Sühan Altay today at 10:00 at TU Wien.

Additionally todays talks within the Vienna Probability Seminar start

later than I have announced yesterday.

Best wishes, Sandra (FAM-office)

------------------------------------------------------------------------

Announcement of Public PhD Thesis Defense at TU Wien

------------------------------------------------------------------------

Tu., 15.01.2019, 10:00, conference room of the Deanery,

TU Wien, 1040, Wiedner Hauptstr. 8, Freihaus, green area, 9th floor

(8th floor, then staircase in the green area)

Sühan Altay (FAM @ TU Wien)

"Interest Rate Modeling and Optimal Trading Portfolios

with Dependence and Partial Information"

(Public PhD Thesis Defense)

For further details (including abstracts) see

https://fam.tuwien.ac.at/events/

------------------------------------------------------------------------

Uni Wien & IST Austria: Vienna Probability Seminar

------------------------------------------------------------------------

Tu., 15.01.2019, 16:30-18:30, room "Besprechungszimmer 2"

Uni Wien, 1090 Wien, Oskar-Morgenstern-Platz 1, 2nd floor

16:30

David Garcia-Zelada (Paris Dauphine, FR)

"A large deviation principle for empirical measures

on Polish spaces"

17:30 (or 5 min later):

Chiranjib Mukherjee (Universität Münster, DE)

"Compactness, large deviations and some applications"

For further details of the Vienna Probability Seminar (including

abstracts) see

https://mathematik.univie.ac.at/forschung/stochastik-und-finanzmathematik/v…

------------------------------------------------------------------------

Joint Seminar: TU Wien, University of Vienna and WU Vienna

------------------------------------------------------------------------

Th., 17.01.2019, 16:30, lecture hall HS13

Uni Wien, 1090 Wien, Oskar-Morgenstern-Platz 1, 2nd floor

Maike Klein (FAM @ TU Wien)

https://fam.tuwien.ac.at/~klein/

"Optimal Stopping Problems with Expectation Constraints"

(Vienna Seminar in Mathematical Finance and Probability)

For further details (including abstracts) see

https://fam.tuwien.ac.at/vs-mfp/

------------------------------------------------------------------------

------------------------------------------------------------------------

Uni Wien & IST Austria: Vienna Probability Seminar

------------------------------------------------------------------------

Tu., 15.01.2019, room "Besprechungszimmer 2"

Uni Wien, 1090 Wien, Oskar-Morgenstern-Platz 1, 2nd floor

15:30-16:30

David Garcia-Zelada (Paris Dauphine, FR)

"A large deviation principle for empirical measures

on Polish spaces"

17:00 - 18:00

Chiranjib Mukherjee (Universität Münster, DE)

"Compactness, large deviations and some applications"

For further details of the Vienna Probability Seminar (including

abstracts) see

https://mathematik.univie.ac.at/forschung/stochastik-und-finanzmathematik/v…

------------------------------------------------------------------------

Joint Seminar: TU Wien, University of Vienna and WU Vienna

------------------------------------------------------------------------

Th., 17.01.2019, 16:30, lecture hall HS13

Uni Wien, 1090 Wien, Oskar-Morgenstern-Platz 1, 2nd floor

Maike Klein (FAM @ TU Wien)

https://fam.tuwien.ac.at/~klein/

"Optimal Stopping Problems with Expectation Constraints"

(Vienna Seminar in Mathematical Finance and Probability)

For further details (including abstracts) see

https://fam.tuwien.ac.at/vs-mfp/

------------------------------------------------------------------------

------------------------------------------------------------------------

WU Public Lecture

------------------------------------------------------------------------

Tu., 8.1.2019, 18:00, Ceremonial Hall 1 / Festsaal 1

WU Wien, 1020, Welthandelsplatz 1, Building LC, ground floor

"The Cost of Destroying the Death Star"

(WU Public Lecture)

Keynote speaker & panellist:

Zach Feinstein (Washington University in St. Louis, US)

Further panellists:

Birgit Rudloff (WU Vienna, AT)

Martin Summer (OeNB, AT)

Moderator:

Stefan Pichler (vice rector, WU Vienna, AT)

For abstract and registration see:

https://wu.at/matters-deathstar or

https://www.facebook.com/events/284338275717020/

To find the room on the WU Campus search for "LC.0.100" on:

http://gis.wu.ac.at/?roomShow=LC.0.100

------------------------------------------------------------------------

Joint Seminar: TU Wien, University of Vienna and WU Vienna

------------------------------------------------------------------------

Th., 10.1.2019, 16:30, lecture hall HS13

Uni Wien, 1090 Wien, Oskar-Morgenstern-Platz 1, 2nd floor

Christian Bayer (WIAS Berlin, DE)

https://www.wias-berlin.de/people/bayerc/

"A regularity structure for rough volatility"

(Vienna Seminar in Mathematical Finance and Probability)

For further details (including abstracts) see

https://fam.tuwien.ac.at/vs-mfp/

------------------------------------------------------------------------

WU Wien, Institute for Statistics and Mathematics

------------------------------------------------------------------------

Fr., 11.01.2019, 09:00, seminar room D4.4.008

WU Wien, 1020, Welthandelsplatz 1, WU Campus, building D4, 4th floor

Zach Feinstein (Washington University in St. Louis, US)

https://engineering.wustl.edu/Profiles/Pages/Zachary-Feinstein.aspx

"Pricing debt in an Eisenberg-Noe

interbank network with comonotonic endowments"

(Research seminar - Statistics and Mathematics)

For further details (including abstracts) see

https://www.wu.ac.at/en/statmath/research/resseminar/

To find the room on the WU Campus search for "D4.4.008" on:

http://gis.wu.ac.at/?roomShow=D4.4.008

------------------------------------------------------------------------

TU Wien, recruitment talks "Mathematische Stochastik"

------------------------------------------------------------------------

As already sent out before christmas holidays, the

recruitment talks for the full professorship in

robability Theory and Mathematical Statistics

("Universitätsprofessur für Mathematische Stochastik")

continue from today to this Wednesday.

For details, including abstract see:

https://fam.tuwien.ac.at/contact/temp/Berufungsvortraege_MSTOCH.pdf

------------------------------------------------------------------------

Dear colleagues,

the researchers

- Mathias Beiglböck and

- Nathanael Berestycki

from University of Vienna and

- Laszlo Erdös and

- Jan Maas

from IST Austria

start a new seminar:

Vienna Probability Seminar

^^^^^^^^^^^^^^^^^^^^^^^^^^

See:

https://mathematik.univie.ac.at/forschung/stochastik-und-finanzmathematik/v…

Talks of this seminar will usually not be posted on the FAM-news

mailinglist (unless talks are within the area of Financial and Actuarial

Mathematics).

In case you are interested in these talks you can subscribe yourself to

the corresponding mailinglist:

https://lists.univie.ac.at/mailman/listinfo/vps

Best wishes,

Sandra

--

Sandra Trenovatz <sandra(a)fam.tuwien.ac.at>

phone +43-1-58801-10511, mobile +43-664-5005638

Financial and Actuarial Mathematics (FAM), https://fam.tuwien.ac.at/

TU Wien, Wiedner Hauptstrasse 8/105-1, 1040 Vienna, Austria

(DVR: 0005886)

Dear friends of FAM & subscribers of FAM-news,

this week seems to be a quiet week for talks in the area of financial

and actuarial mathematics - nevertheless it will not be quiet at all.

The recruitment talks for the full professorship in Probability Theory

and Mathematical Statistics ("Universitätsprofessur für Mathematische

Stochastik") at TU Wien start this Tuesday. Stochastics/Probability

theory is important for many different fields of science and technology

- therefore we announce these talks.

As the next two weeks there will be (most probably) no talks I already

now wish you a Merry Christmas and a prosperous New Year 2019!

Sandra (Sandra Trenovatz, FAM, http://fam.tuwien.ac.at/)

---------------------------------------------------------------------

TU Wien, recruitment talks "Mathematische Stochastik"

---------------------------------------------------------------------

Tu., 18.12.2018, 10:30-12:30, lecture hall HS 17 Friedrich Hartmann

TU Wien, 1040, Karlsplatz 13, staircase 7, 3rd floor

Alexandre Stauffer (University of Bath)

https://sites.google.com/site/alexandrestauffer/

"Random aggregation processes: Long-time behavior,

phase transition and dendritic formation"

For details, including abstract see:

https://fam.tuwien.ac.at/contact/temp/Berufungsvortraege_MSTOCH.pdf

To find the lecture hall HS17 in the main building of TU Wien see:

https://fam.tuwien.ac.at/contact/temp/HS17.png

-----

Overview of all recruitment talks for the

full professorship in Probability Theory and Mathematical Statistics

("Universitätsprofessur für Mathematische Stochastik"):

Tu., 18.12.2018, HS 17:

10:30 Alexandre Stauffer

Mo., 07.01.2019, FH 3:

08:30 Omer Angel

10:30 Mykhaylo Shkolnikov

14:00 Erika Hausenblas

16:00 Johannes Muhle-Karbe

Tu., 08.01.2019, FH 2:

10:00 Nicolas Perkowski

13:30 Fabio Toninelli

16:00 Arnulf Jentzen

We., 09.01.2019, FH 3:

08:30 Noam Berger

10:30 Matthias Erbar

---------------------------------------------------------------------

------------------------------------------------------------------------

University of Vienna, Dept. of Statistics and Decision Support Systems

------------------------------------------------------------------------

Mo., 10.12.2018, 16:45, lecture hall HS 7 (#1.303)

Uni Wien, 1090 Vienna, Oskar-Morgenstern-Platz 1, 1st floor

Damian Kozbur (Universität Zurich)

https://www.econ.uzh.ch/en/people/faculty/kozbur.html

"Inference for Dependent Data with Cluster Learning"

(ISOR Colloquium)

The seminar is preceded by tea and coffee with the speaker in the ISOR

meeting room (#6.511, 6th floor) at 16.15.

For further details (including abstracts) see

https://isor.univie.ac.at/isor-colloquium/

------------------------------------------------------------------------

WU Wien, Institute for Finance, Banking and Insurance

------------------------------------------------------------------------

We., 12.12.2018, 11:00-12:15, room D4.4.008

WU Wien, 1020, Welthandelsplatz 1, WU Campus, building D4, ground floor

Paul Pelzl (VU Amsterdam & Tinbergen Institute)

https://research.vu.nl/en/persons/paul-pelzl

"Capital Regulations and Credit Line Management

during Crisis Times"

(Finance Brown Bag Seminar)

For further details (including abstracts) see

https://www.wu.ac.at/en/finance/research/brown-bag-seminar/

To find the room on the WU Campus search for "D4.4.008" on:

http://gis.wu.ac.at/?roomShow=D4.4.008

-------------------------------------------------------------------------

University of Vienna, Deptartment of Finance

------------------------------------------------------------------------

We., 12.12.2018, 11:45-12:45, seminar room 6

Uni Wien, 1090 Vienna, Oskar-Morgenstern-Platz 1, 1st floor

Guillaume Vuillemey (HEC Paris)

https://sites.google.com/site/guillaumevuillemey/

"Completing Markets with Contracts: Evidence

from the First Central Clearing Counterparty"

(Brown Bag Seminar)

For further details (including abstracts) see

http://finance.univie.ac.at/en/research/brown-bag-seminar/

------------------------------------------------------------------------

Joint Seminar: TU Wien, University of Vienna and WU Vienna

------------------------------------------------------------------------

Th., 13.12.2018, 16:30, lecture hall HS13

Uni Wien, 1090 Wien, Oskar-Morgenstern-Platz 1, 2nd floor

Oleg I. Klesov (National Technical University of Ukraine)

http://matan.kpi.ua/en/people/klesov/

"Law of the iterated logarithm for inverse subordinators

and some applications in risk models"

(Vienna Seminar in Mathematical Finance and Probability)

For further details (including abstracts) see

https://fam.tuwien.ac.at/vs-mfp/

------------------------------------------------------------------------

------------------------------------------------------------------------

University of Vienna, Dept. of Statistics and Decision Support Systems

------------------------------------------------------------------------

Mo., 10.12.2018, 16:45, lecture hall HS 7 (#1.303)

Uni Wien, 1090 Vienna, Oskar-Morgenstern-Platz 1, 1st floor

Damian Kozbur (Universität Zurich)

https://www.econ.uzh.ch/en/people/faculty/kozbur.html

"Inference for Dependent Data with Cluster Learning"

(ISOR Colloquium)

The seminar is preceded by tea and coffee with the speaker in the ISOR

meeting room (#6.511, 6th floor) at 16.15.

For further details (including abstracts) see

https://isor.univie.ac.at/isor-colloquium/

------------------------------------------------------------------------

WU Wien, Institute for Finance, Banking and Insurance

------------------------------------------------------------------------

We., 12.12.2018, 11:00-12:15, room D4.4.008

WU Wien, 1020, Welthandelsplatz 1, WU Campus, building D4, ground floor

Paul Pelzl (VU Amsterdam & Tinbergen Institute)

https://research.vu.nl/en/persons/paul-pelzl

"Capital Regulations and Credit Line Management during Crisis Times"

(Finance Brown Bag Seminar)

For further details (including abstracts) see

https://www.wu.ac.at/en/finance/research/brown-bag-seminar/

To find the room on the WU Campus search for "D4.4.008" on:

http://gis.wu.ac.at/?roomShow=D4.4.008

-------------------------------------------------------------------------

University of Vienna, Deptartment of Finance

------------------------------------------------------------------------

We., 12.12.2018, 11:45-12:45, seminar room 6

Uni Wien, 1090 Vienna, Oskar-Morgenstern-Platz 1, 1st floor

Guillaume Vuillemey (HEC Paris)

http://www.hec.edu/Faculty-Research/Faculty-Directory/VUILLEMEY-Guillaume

"Completing Markets with Contracts:

Evidence from the First Central Clearing Counterparty"

(Brown Bag Seminar)

For further details (including abstracts) see

http://finance.univie.ac.at/en/research/brown-bag-seminar/

------------------------------------------------------------------------

Joint Seminar: TU Wien, University of Vienna and WU Vienna

------------------------------------------------------------------------

Th., 13.12.2018, 16:30, lecture hall HS13

Uni Wien, 1090 Wien, Oskar-Morgenstern-Platz 1, 2nd floor

Oleg I. Klesov (National Technical University of Ukraine)

http://matan.kpi.ua/en/people/klesov/

"Law of the iterated logarithm for inverse subordinators

and some applications in risk models"

(Vienna Seminar in Mathematical Finance and Probability)

For further details (including abstracts) see

https://fam.tuwien.ac.at/vs-mfp/

------------------------------------------------------------------------

------------------------------------------------------------------------

University of Vienna, Dept. of Statistics and Decision Support Systems

------------------------------------------------------------------------

Mo., 3.12.2018, 16:45, lecture room 7 (#1.303)

Uni Wien, 1090 Vienna, Oskar-Morgenstern-Platz 1, 1st floor

Mathias Pohl (University of Vienna)

https://fec.univie.ac.at/researchers/mathias-pohl/

"Robust risk aggregation with neural networks"

(joint work with Stephan Eckstein and Michael Kupper)

(ISOR Colloquium)

The seminar is preceded by tea and coffee with the speaker in the ISOR

meeting room (#6.511, 6th floor) at 16.15.

For further details (including abstracts) see

https://isor.univie.ac.at/isor-colloquium/

------------------------------------------------------------------------

Veranstaltungsreihe "Actuarial Modelling Club"

------------------------------------------------------------------------

Tu., 04.12.2018, 16:30, lecture hall: GM 3 Vortmann Hörsaal

TU Wien, 1060, Getreidemarkt 9, Plus Energie Büro Hochhaus, 2. Stock

Onnen Siems, Carina Götzen (Meyerthole Siems Kohlruss, DE)

Praxisbericht "Aktuarielle Analyse von

großen Telematikdatenmengen (Big Data)"

(Actuarial Modelling Club)

For further details (including abstracts) and registration see

https://fam.tuwien.ac.at/vr/

------------------------------------------------------------------------

University of Vienna, Deptartment of Finance

------------------------------------------------------------------------

We., 5.12.2018, 11:45-12:45, seminar room 6

Uni Wien, 1090 Vienna, Oskar-Morgenstern-Platz 1, 1st floor

Anton van Boxtel (University of Vienna)

https://sites.google.com/site/antonvanboxtel/

"Credit Market Competition and Liquidity"

(Brown Bag Seminar)

For further details (including abstracts) see

http://finance.univie.ac.at/en/research/brown-bag-seminar/

------------------------------------------------------------------------

Joint Seminar: TU Wien, University of Vienna and WU Vienna

------------------------------------------------------------------------

Th., 06.12.2018, 16:30, lecture hall HS13

Uni Wien, 1090 Wien, Oskar-Morgenstern-Platz 1, 2nd floor

Halil Mete Soner (ETH Zürich, CH)

https://people.math.ethz.ch/~hmsoner/

"Pricing-hedging Duality"

(Vienna Seminar in Mathematical Finance and Probability)

For further details (including abstracts) see

https://fam.tuwien.ac.at/vs-mfp/

------------------------------------------------------------------------

TU Wien, Faculty of Mathematics and Geoinformation

------------------------------------------------------------------------

Fr., 07.12.2018, 11:00, seminar room DA grün 05,

TU Wien, 1040, Wiedner Hauptstr. 8, Freihaus, 5th floor, green area

Julia Eisenberg (TU Wien, AT & Univ. Liverpool, UK)

https://fam.tuwien.ac.at/~jeisenbe/

"The time value of money in the actuarial framework"

(Vorstellungsvortrag vor angestrebter Habilitation)

For further details (including abstracts) see

https://fam.tuwien.ac.at/events/

------------------------------------------------------------------------

------------------------------------------------------------------------

Joint Seminar: TU Wien, University of Vienna and WU Vienna

------------------------------------------------------------------------

Th., 29.11.2018, 16:30, lecture hall HS13

Uni Wien, 1090 Wien, Oskar-Morgenstern-Platz 1, 2nd floor

Andrey Pilipenko (National Technical University of Ukraine)

https://www.imath.kiev.ua/~apilip/

"Functional limit theorems for perturbed random walks"

(Vienna Seminar in Mathematical Finance and Probability)

For further details (including abstracts) see

https://fam.tuwien.ac.at/vs-mfp/

------------------------------------------------------------------------

WU Wien, Institute for Statistics and Mathematics

------------------------------------------------------------------------

Fr., 30.11.2018, 09:00, seminar room D4.4.008

WU Wien, 1020, Welthandelsplatz 1, WU Campus, building D4, 4th floor

Alexander McNeil (University of York, UK)

https://www.york.ac.uk/management/staff/amcneil/

"Spectral backtests of forecast distributions

with application to risk management"

(Research seminar - Statistics and Mathematics)

For further details (including abstracts) see

https://www.wu.ac.at/en/statmath/research/resseminar/

To find the room on the WU Campus search for "D4.4.008" on:

http://gis.wu.ac.at/?roomShow=D4.4.008

------------------------------------------------------------------------

------------------------------------------------------------------------

University of Vienna, Dept. of Statistics and Decision Support Systems

------------------------------------------------------------------------

Mo., 19.11.2018, 16:45, lecture hall HS 7

Uni Wien, 1090 Vienna, Oskar-Morgenstern-Platz 1, 1st floor

Peter Filzmoser (TU Wien)

http://file.statistik.tuwien.ac.at/filz/

"Robust estimators of maximum association"

(ISOR Colloquium)

The seminar is preceded by tea and coffee with the speaker in the ISOR

meeting room (6.511, 6th floor) at 16.15.

For further details (including abstracts) see

https://isor.univie.ac.at/isor-colloquium/

------------------------------------------------------------------------

Joint Seminar: TU Wien, University of Vienna and WU Vienna

------------------------------------------------------------------------

Th., 22.11.2018, 16:30, lecture hall HS13

Uni Wien, 1090 Wien, Oskar-Morgenstern-Platz 1, 2nd floor

Thilo Meyer-Brandis (LMU Munich, DE)

http://www.fm.mathematik.uni-muenchen.de/personen/professors/meyer_brandis/

"Contagion and Systemic Risk

in Heterogeneous Financial Networks"

(Vienna Seminar in Mathematical Finance and Probability)

For further details (including abstracts) see

https://fam.tuwien.ac.at/vs-mfp/

------------------------------------------------------------------------

WU Wien, Institute for Statistics and Mathematics

------------------------------------------------------------------------

Fr., 23.11.2018, 9:00, seminar room D4.4.008

WU Wien, 1020, Welthandelsplatz 1, WU Campus, building D4, 4th floor

Johannes Heiny (University of Aarhus, DK)

"Assessing the dependence of high-dimensional time

series via autocovariances and autocorrelations"

(Research seminar - Statistics and Mathematics)

For further details (including abstracts) see

https://www.wu.ac.at/en/statmath/research/resseminar/

To find the room on the WU Campus search for "D4.4.008" on:

http://gis.wu.ac.at/?roomShow=D4.4.008

------------------------------------------------------------------------

------------------------------------------------------------------------

WU Wien, Institute for Statistics and Mathematics

------------------------------------------------------------------------

Fr., 16.11.2018, 09:00, seminar room D4.4.008

WU Wien, 1020, Welthandelsplatz 1, WU Campus, building D4, 4th floor

Clara Grazian (University of Oxford)

https://sites.google.com/site/claragrazian/home

"Bayesian analysis of semiparametric copula models"

(Research seminar - Statistics and Mathematics)

For further details (including abstracts) see

https://www.wu.ac.at/en/statmath/research/resseminar/

To find the room on the WU Campus search for "D4.4.008" on:

http://gis.wu.ac.at/?roomShow=D4.4.008

------------------------------------------------------------------------

WU Wien, Institute for Statistics and Mathematics

------------------------------------------------------------------------

Fr., 16.11.2018, 11:00, seminar room D4.4.008

WU Wien, 1020, Welthandelsplatz 1, WU Campus, building D4, 4th floor

Christa Cuchiero (University of Vienna)

https://www.mat.univie.ac.at/~cuchiero/

"Contemporary stochastic volatility modeling

- theory and empirics"

(Research seminar - Statistics and Mathematics)

For further details (including abstracts) see

https://www.wu.ac.at/en/statmath/research/resseminar/

To find the room on the WU Campus search for "D4.4.008" on:

http://gis.wu.ac.at/?roomShow=D4.4.008

------------------------------------------------------------------------

Vienna Graduate School of Finance (VGSF)

------------------------------------------------------------------------

Fr., 16.11.2018, 11:00, room D3.0.225

WU Wien, 1020, Welthandelsplatz 1, WU Campus, building D3, ground floor

Adrian Buss (INSEAD)

https://www.insead.edu/faculty-research/faculty/adrian-buss

"The Implications of Financial Innovation for

Capital Markets and Household Welfare"

(Finance Research Seminar)

For further details (including abstracts) see

http://www.vgsf.ac.at/events/finance-research-seminar/

To find the room on the WU Campus search for "D3.0.225" on:

http://gis.wu.ac.at/?roomShow=D3.0.225

------------------------------------------------------------------------

------------------------------------------------------------------------

Announcement of Public PhD Thesis Defense at University of Vienna

------------------------------------------------------------------------

Mo., 2.7.2018, 11:00, seminar room 2

Uni Wien, 1090 Wien, Oskar-Morgenstern-Platz 1, 1st floor

Mathias Pohl (University of Vienna)

"Robust Portfolio Optimization and

Dimensional Analysis in Finance"

(Public PhD Thesis Defense)

For further details see

https://fam.tuwien.ac.at/contact/temp/20180702_phd-defense_pohl.pdf

------------------------------------------------------------------------

Joint Seminar: TU Wien, University of Vienna and WU Vienna

------------------------------------------------------------------------

Th., 4.7.2018, 16:30, seminar room DC rot 07

TU Wien, 1040, Wiedner Hauptstr. 8, Freihaus, 7th floor, red area

Khaled Bahlali (Université de Toulon)

https://www.hindawi.com/28918560/

"t.b.a."

(Vienna Seminar in Mathematical Finance and Probability)

For further details (including abstracts) see

https://fam.tuwien.ac.at/vs-mfp/

------------------------------------------------------------------------

TU Wien - VISS 2018 - registration ends on Monday, July 2

------------------------------------------------------------------------

VISS 2018 - Vienna International Summer School

"Machine Learning Methods and Data Analytics in Risk and Insurance"

TU Wien, Mon-Fri, July 9 - 13, 2018

https://fam.tuwien.ac.at/viss2018/

Main speakers:

Prof. Dr. Gareth W. PETERS, Heriot-Watt University, Edinburgh

Prof. Dr. Pavel V. SHEVCHENKO, Macquarie University, Sydney

Special invited lectures:

Prof. Dr. Josef TEICHMANN, ETH Zurich

Prof. Dr. Allan HANBURY, TU Wien

Registration possible until Monday, July 2

https://fam.tuwien.ac.at/viss2018/registration.php

------------------------------------------------------------------------

------------------------------------------------------------------------

Joint Seminar: TU Wien, University of Vienna and WU Vienna

------------------------------------------------------------------------

Th., 25.10.2018, 16:30, lecture hall HS13

Uni Wien, 1090 Wien, Oskar-Morgenstern-Platz 1, 2nd floor

Dominik Norgilas (University of Warwick, UK)

https://warwick.ac.uk/fac/sci/statistics/staff/research_students/norgilas/

"The left-curtain martingale coupling

and the American put in the presence of atoms"

(Vienna Seminar in Mathematical Finance and Probability)

For further details (including abstracts) see

https://fam.tuwien.ac.at/vs-mfp/

------------------------------------------------------------------------

------------------------------------------------------------------------

Joint Seminar: TU Wien, University of Vienna and WU Vienna

------------------------------------------------------------------------

Th., 18.10.2018, 16:30, seminar room SR11

Uni Wien, 1090 Wien, Oskar-Morgenstern-Platz 1, 2nd floor

Johannes Wiesel (University of Oxford, UK)

https://www.maths.ox.ac.uk/people/johannes.wiesel

"Statistical estimation of superhedging prices"

(Vienna Seminar in Mathematical Finance and Probability)

For further details (including abstracts) see

https://fam.tuwien.ac.at/vs-mfp/

------------------------------------------------------------------------

WU Wien, Institute for Statistics and Mathematics

------------------------------------------------------------------------

Fr., 19.10.2018, 09:00, seminar room D4.4.008

WU Wien, 1020, Welthandelsplatz 1, WU Campus, building D4, 4th floor

Matthias Fengler (University of St. Gallen, CH)

https://www.alexandria.unisg.ch/persons/2894

"Textual Sentiment, Option Characteristics,

and Stock Return Predictability"

(Research seminar - Statistics and Mathematics)

For further details (including abstracts) see

https://www.wu.ac.at/en/statmath/research/resseminar/

To find the room on the WU Campus search for "D4.4.008" on:

http://gis.wu.ac.at/?roomShow=D4.4.008

------------------------------------------------------------------------

Vienna Graduate School of Finance (VGSF)

------------------------------------------------------------------------

Fr., 19.10.2018, 11:00, room D3.0.225

WU Wien, 1020, Welthandelsplatz 1, WU Campus, building D3, ground floor

Suleyman Basak (London Business School, UK)

http://www.suleymanbasak.com

"Asset Prices and No-Dividend Stocks"

(Finance Research Seminar)

For further details (including abstracts) see

http://www.vgsf.ac.at/events/finance-research-seminar/

To find the room on the WU Campus search for "D3.0.225" on:

http://gis.wu.ac.at/?roomShow=D3.0.225

------------------------------------------------------------------------

To Whom it May Concern:

after a summer break FAM-news will again regularly announce talks &

events in the area of Financial and Actuarial Mathematics (FAM) in

Vienna. Sometimes also a few others.

In case you have new colleagues who might be intersted in the FAM-news

mailinglist please forward this e-mail to them, so they can subscribe:

https://fam.tuwien.ac.at/mailman/listinfo/fam-news

Best wishes, Sandra

(Sandra Trenovatz, FAM-office, fam(a)fam.tuwien.ac.at)

------------------------------------------------------------------------

WU Wien, Institute for Statistics and Mathematics

------------------------------------------------------------------------

Fr., 12.10.2018, 09:00, seminar room D4.4.008

WU Wien, 1020, Welthandelsplatz 1, WU Campus, building D4, 4th floor

Walter Farkas (University of Zurich)

https://people.math.ethz.ch/~farkas/

"Intrinsic Risk Measures"

(Research seminar - Statistics and Mathematics)

For further details (including abstracts) see

https://www.wu.ac.at/en/statmath/research/resseminar/

To find the room on the WU Campus search for "D4.4.008" on:

http://gis.wu.ac.at/?roomShow=D4.4.008

------------------------------------------------------------------------

IST Austria, talk of new professor for Stochastics of Univ. of Vienna

------------------------------------------------------------------------

Tu., 09.10.2018, 16:00, Big Seminar room I21.EG.101 (ground floor)

IST Austria, 3400 Klosterneuburg, Am Campus 1, Office Building West

Nathanael Berestycki (University of Vienna)

https://homepage.univie.ac.at/nathanael.berestycki/

"Dimers and Imaginary Geometry"

(Formal Sciences Seminar)

For further details (including abstracts) see

https://ist.ac.at/index.php?id=2480&event_id=1399

Shuttle bus from U4 Heiligenstadt to IST Austria:

https://ist.ac.at/campus-life/shuttle-bus/

------------------------------------------------------------------------

------------------------------------------------------------------------

WU Vienna - Austrian Stochastics Days

------------------------------------------------------------------------

7th Austrian Stochastics Days 2018

WU Vienna, Thu-Fri, September 13-14, 2018

http://asd2018.wu.ac.at/

Submission is possible until August 15th, 2018

(earlier submission is very welcome).

Registration is madatory but free

and possible until August 25th, 2018.

------------------------------------------------------------------------

TU Wien - Praxistage 2018

------------------------------------------------------------------------

Praxis der Finanz- und Versicherungsmathematik 2018

(inkl. Berufsständisches Seminar der AVÖ)

TU Wien, Di.-Mi., 25.-26. September 2018

https://fam.tuwien.ac.at/events/praxisFVM2018/

------------------------------------------------------------------------

Save the date / next year: VCMF 2019

------------------------------------------------------------------------

2nd Vienna Congress on Mathematical Finance 2019

& VCMF Educational Workshop

(jointly organised by WU Wien, TU Wien and University of Vienna)

WU Vienna, Mon-Fri, September 9-13, 2019

https://fam.tuwien.ac.at/vcmf2019/

------------------------------------------------------------------------

------------------------------------------------------------------------

Uni Wien, Vortragsreihe "Finanzmathematik und Data Science"

------------------------------------------------------------------------

We., 27.6.2018, 17:45-19:15, lecture hall / Hörsaal 13

Uni Wien, 1090 Wien, Oskar-Morgenstern-Platz 1, 2nd floor

Christoph Krischanitz (Arithmetica)

"Die vielfältigen Anwendungen von Datenanalyse

und Simulationstechniken in der Wirtschaft"

For further details see

http://www.mat.univie.ac.at/~mfulmek/kobm2018.shtml

------------------------------------------------------------------------

Joint Seminar: TU Wien, University of Vienna and WU Vienna

------------------------------------------------------------------------

Th., 28.6.2018, 16:30, seminar room DC rot 07

TU Wien, 1040, Wiedner Hauptstr. 8, Freihaus, 7th floor, red area

Archil Gulisashvili (Ohio University, US)

https://www.ohio.edu/cas/math/contact/profiles.cfm?profile=gulisash

"Volterra type fractional stochastic volatility models.

Small-noise and small-time asymptotic formulas

for the implied volatility"

(Vienna Seminar in Mathematical Finance and Probability)

For further details (including abstracts) see

https://fam.tuwien.ac.at/vs-mfp/

------------------------------------------------------------------------

------------------------------------------------------------------------

Uni Wien, Vortragsreihe "Finanzmathematik und Data Science"

------------------------------------------------------------------------

We., 20.6.2018, 17:45-19:15, lecture hall / Hörsaal 13

Uni Wien, 1090 Wien, Oskar-Morgenstern-Platz 1, 2nd floor

Ulrike Freisleben-Hof (RLB NÖ-Wien)

"Banken ein Jahrzehnt nach der Finanzkrise im Zeitalter

der Digitalisierung. Ein Bericht aus der Praxis"

For further details see

http://www.mat.univie.ac.at/~mfulmek/kobm2018.shtml

------------------------------------------------------------------------

Joint Seminar: TU Wien, University of Vienna and WU Vienna

------------------------------------------------------------------------

Th., 21.6.2018, 16:30, seminar room DC rot 07

TU Wien, 1040, Wiedner Hauptstr. 8, Freihaus, 7th floor, red area

Oleg Szehr (University of Vienna)

"Supervised learning and optimal transport"

(Vienna Seminar in Mathematical Finance and Probability)

For further details (including abstracts) see

https://fam.tuwien.ac.at/vs-mfp/

------------------------------------------------------------------------

------------------------------------------------------------------------

Uni Wien, Vortragsreihe "Finanzmathematik und Data Science"

------------------------------------------------------------------------

We., 13.6.2018, 17:45-19:15, lecture hall / Hörsaal 13

Uni Wien, 1090 Wien, Oskar-Morgenstern-Platz 1, 2nd floor

Richard Warnung (BAWAG P.S.K)

"Kreditrisikomodellierung mit Illustrationen in R"

For further details see

http://www.mat.univie.ac.at/~mfulmek/kobm2018.shtml

------------------------------------------------------------------------

Joint Seminar: TU Wien, University of Vienna and WU Vienna

------------------------------------------------------------------------

Th., 14.6.2018, 16:30, seminar room DC rot 07

TU Wien, 1040, Wiedner Hauptstr. 8, Freihaus, 7th floor, red area

Stephan Eckstein (University of Konstanz, DE)

https://www.mathematik.uni-konstanz.de/kupper/team/stephan-eckstein/