To Whom it May Concern,

additionally to a talk this week we announce a few events of research

and cooperation partners as well as the "Vienna Congress on Mathematical

Finance (VCMF 2019)" co-organised by FAM @ TU Wien.

Best wishes, Sandra (Trenovatz)

------------------------------------------------------------------------

Veranstaltungsreihe "Actuarial Modelling Club"

------------------------------------------------------------------------

Th., 21.3.2019, 17:00, Freihaus Hörsaal 5

TU Wien, 1040, Wiedner Hauptstraße 8-10 , 2. Stock, grüner Bereich

Dr. Gerold Petritsch (EVN)

"Über den aktuariellen Tellerrand hinaus:

Data Science als Erfolgsfaktor in der Energiewirtschaft"

(Actuarial Modelling Club)

For further details (including abstracts) and registration see

https://fam.tuwien.ac.at/vr/

------------------------------------------------------------------------

------------------------------------------------------------------------

MathFinance - Frankfurt, April 2019

------------------------------------------------------------------------

MathFinance Conference

Frankfurt, April 8-9, 2019

MathFinance hosts the annual Conference in Frankfurt which is tailored

to the European finance community. Providing cutting-edge research and

brand new practical applications, the conference is intended for

practitioners in the areas of trading, quantitative or derivative

research, risk and asset management, insurance as well as for academics

studying or researching in the field of financial mathematics.

https://www.mathfinance.com/events/mathfinance-conference/

------------------------------------------------------------------------

Optimal Transport - Vienna, May/June 2019

------------------------------------------------------------------------

Thematic Programme "Optimal Transport"

The program brings together researchers working on Optimal Transport in

diverse areas, such as stochastic analysis, mathematical finance,

analysis in singular spaces, geometric inequalities, gradient flows,

optimal random matching, optimal transport for density matrices,

numerical methods, computer vision, and machine learning. The aim of the

proposed ESI programme is to establish interactions, encourage new

collaborations, and identify synergies between these different disciplines.

May 6-10: Introductory School on Optimal Transport

May 13-17: Workshop 1: Optimal Transport: from Geometry to Numerics

June 3-7: Workshop 2: Opt. Transport in Analysis and Probability

http://pub.ist.ac.at/~jmaas/ESI_OT2019/

------------------------------------------------------------------------

AMaMeF - Paris, June 2019

------------------------------------------------------------------------

9th General AMaMeF Conference

Paris, June 11-14, 2019 in Paris

AMaMeF, acronym for Advanced Mathematical Methods in Finance, is a

European network of research promoting the exchange and diffusion of

knowledge in the field of Mathematical Finance. Under the auspices of

AMaMeF numerous conferences, workshops and other scientific activities

have been organized. Among these the General AMaMeF Conferences have

been the biggest, and they are currently organized in a roughly

two-yearly schedule.

https://9amamef.sciencesconf.org

------------------------------------------------------------------------

VCMF 2019 - Vienna, September 2019

------------------------------------------------------------------------

2nd Vienna Congress on Mathematical Finance 2019

& VCMF Educational Workshop

WU Vienna, Mon-Fri, September 9-13, 2019,

jointly organised by WU Wien, TU Wien and University of Vienna

Submission of abstracts as well as registration is already possible:

https://fam.tuwien.ac.at/vcmf2019/

The VCMF 2019 follows the successful previous edition, VCMF 2016, with

240 attendees, 83 talks and 28 poster presentations.

------------------------------------------------------------------------

--------------------------------------------------------------------

Announcement of Public PhD Thesis Defense at TU Wien

--------------------------------------------------------------------

We., 13.3.2019, 14:00, conference room of the Deanery,

TU Wien, 1040, Wiedner Hauptstr. 8, Freihaus, green area, 9th floor

(8th floor, then staircase in the green area)

Christiane Elgert (FAM @ TU Wien)

"Theory of Distribution-Constrained Optimization Problems"

(Public PhD Thesis Defense)

For further details (including abstracts) see

https://fam.tuwien.ac.at/events/

--------------------------------------------------------------------

------------------------------------------------------------------------

PDE Afternoon at TU Wien

------------------------------------------------------------------------

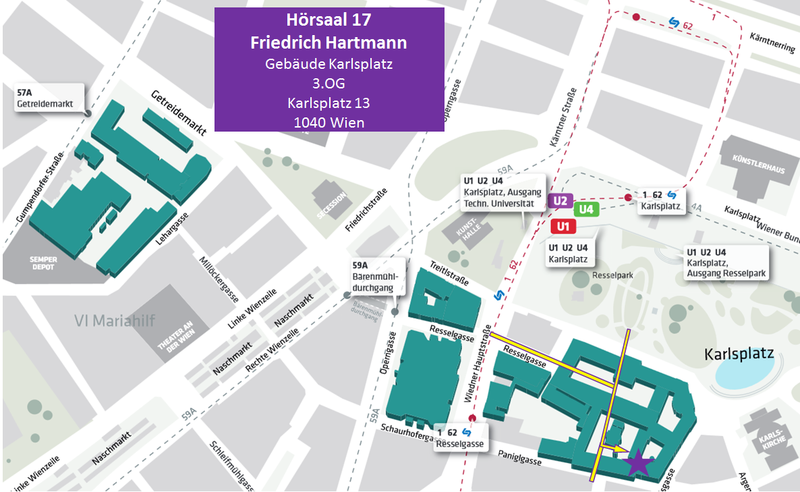

We., 06.03.2019, 15:30 bis 16:00, HS 17 Friedrich,

TU Wien, 1040, Karlsplatz 13, main building, staircase VII, 3rd floor

Gudmund Pammer (TU Wien)

"Stability of the weak transport / continuity

of super-hedging in finance"

(PDE Afternoon)

For further details see

https://www.univie.ac.at/sfb65/#!/public/events/details/?type=1&id=380

------------------------------------------------------------------------

TU ForMath — Forum Mathematik

------------------------------------------------------------------------

Th., 7.3.2019, 18:00 - 19:00, Freihaus Hörsaal 3

TU Wien, 1040, Wiedner Hauptstr. 8, Freihaus, 2nd floor, yellow area

Johannes Morgenbesser (Österreichische Nationalbank)

"Mathematics undercover: Die Mathematik hinter Blockchain und Bitcoin"

For further information see:

https://www.tuformath.at/vortraege/

------------------------------------------------------------------------

------------------------------------------------------------------------

Talks at University of Vienna

------------------------------------------------------------------------

Tu., 19.02.2019, 16:30, lecture hall HS13

Uni Wien, 1090 Wien, Oskar-Morgenstern-Platz 1, 2nd floor

Nicolas Juillet (Université de Strasbourg)

"Excursions and Transport"

Abstract:

Transport on the real line for power of the distance $d^p$ cost is

well-known especially when p>1 where the canonical quantile transport is

the unique optimal transport. For p=1 it is not unique and for p<1 it is

not optimal anymore and there is no uniqueness anymore. However, I will

present a natural transport problem providing a solution that catches in

a canonical way the transport behavior for p<1.

(https://mathematik.univie.ac.at/newsevents/nachrichtenvolldarstellung/news/…)

------------------------------------------------------------------------

------------------------------------------------------------------------

Joint Seminar: TU Wien, University of Vienna and WU Vienna

------------------------------------------------------------------------

Th., 24.01.2019, 16:30, lecture hall HS13

Uni Wien, 1090 Wien, Oskar-Morgenstern-Platz 1, 2nd floor

Nathael Gozlan (Université Paris 5 - René Descartes)

https://sites.google.com/view/nathaelgozlanmath

"Optimal transport for barycentric transport costs"

(Vienna Seminar in Mathematical Finance and Probability)

For further details (including abstracts) see

https://fam.tuwien.ac.at/vs-mfp/

------------------------------------------------------------------------

To whom it may concern,

I appologize for the second mailing this week, but I forgot to send out

the public PhD theses defense of Sühan Altay today at 10:00 at TU Wien.

Additionally todays talks within the Vienna Probability Seminar start

later than I have announced yesterday.

Best wishes, Sandra (FAM-office)

------------------------------------------------------------------------

Announcement of Public PhD Thesis Defense at TU Wien

------------------------------------------------------------------------

Tu., 15.01.2019, 10:00, conference room of the Deanery,

TU Wien, 1040, Wiedner Hauptstr. 8, Freihaus, green area, 9th floor

(8th floor, then staircase in the green area)

Sühan Altay (FAM @ TU Wien)

"Interest Rate Modeling and Optimal Trading Portfolios

with Dependence and Partial Information"

(Public PhD Thesis Defense)

For further details (including abstracts) see

https://fam.tuwien.ac.at/events/

------------------------------------------------------------------------

Uni Wien & IST Austria: Vienna Probability Seminar

------------------------------------------------------------------------

Tu., 15.01.2019, 16:30-18:30, room "Besprechungszimmer 2"

Uni Wien, 1090 Wien, Oskar-Morgenstern-Platz 1, 2nd floor

16:30

David Garcia-Zelada (Paris Dauphine, FR)

"A large deviation principle for empirical measures

on Polish spaces"

17:30 (or 5 min later):

Chiranjib Mukherjee (Universität Münster, DE)

"Compactness, large deviations and some applications"

For further details of the Vienna Probability Seminar (including

abstracts) see

https://mathematik.univie.ac.at/forschung/stochastik-und-finanzmathematik/v…

------------------------------------------------------------------------

Joint Seminar: TU Wien, University of Vienna and WU Vienna

------------------------------------------------------------------------

Th., 17.01.2019, 16:30, lecture hall HS13

Uni Wien, 1090 Wien, Oskar-Morgenstern-Platz 1, 2nd floor

Maike Klein (FAM @ TU Wien)

https://fam.tuwien.ac.at/~klein/

"Optimal Stopping Problems with Expectation Constraints"

(Vienna Seminar in Mathematical Finance and Probability)

For further details (including abstracts) see

https://fam.tuwien.ac.at/vs-mfp/

------------------------------------------------------------------------

------------------------------------------------------------------------

Uni Wien & IST Austria: Vienna Probability Seminar

------------------------------------------------------------------------

Tu., 15.01.2019, room "Besprechungszimmer 2"

Uni Wien, 1090 Wien, Oskar-Morgenstern-Platz 1, 2nd floor

15:30-16:30

David Garcia-Zelada (Paris Dauphine, FR)

"A large deviation principle for empirical measures

on Polish spaces"

17:00 - 18:00

Chiranjib Mukherjee (Universität Münster, DE)

"Compactness, large deviations and some applications"

For further details of the Vienna Probability Seminar (including

abstracts) see

https://mathematik.univie.ac.at/forschung/stochastik-und-finanzmathematik/v…

------------------------------------------------------------------------

Joint Seminar: TU Wien, University of Vienna and WU Vienna

------------------------------------------------------------------------

Th., 17.01.2019, 16:30, lecture hall HS13

Uni Wien, 1090 Wien, Oskar-Morgenstern-Platz 1, 2nd floor

Maike Klein (FAM @ TU Wien)

https://fam.tuwien.ac.at/~klein/

"Optimal Stopping Problems with Expectation Constraints"

(Vienna Seminar in Mathematical Finance and Probability)

For further details (including abstracts) see

https://fam.tuwien.ac.at/vs-mfp/

------------------------------------------------------------------------

------------------------------------------------------------------------

WU Public Lecture

------------------------------------------------------------------------

Tu., 8.1.2019, 18:00, Ceremonial Hall 1 / Festsaal 1

WU Wien, 1020, Welthandelsplatz 1, Building LC, ground floor

"The Cost of Destroying the Death Star"

(WU Public Lecture)

Keynote speaker & panellist:

Zach Feinstein (Washington University in St. Louis, US)

Further panellists:

Birgit Rudloff (WU Vienna, AT)

Martin Summer (OeNB, AT)

Moderator:

Stefan Pichler (vice rector, WU Vienna, AT)

For abstract and registration see:

https://wu.at/matters-deathstar or

https://www.facebook.com/events/284338275717020/

To find the room on the WU Campus search for "LC.0.100" on:

http://gis.wu.ac.at/?roomShow=LC.0.100

------------------------------------------------------------------------

Joint Seminar: TU Wien, University of Vienna and WU Vienna

------------------------------------------------------------------------

Th., 10.1.2019, 16:30, lecture hall HS13

Uni Wien, 1090 Wien, Oskar-Morgenstern-Platz 1, 2nd floor

Christian Bayer (WIAS Berlin, DE)

https://www.wias-berlin.de/people/bayerc/

"A regularity structure for rough volatility"

(Vienna Seminar in Mathematical Finance and Probability)

For further details (including abstracts) see

https://fam.tuwien.ac.at/vs-mfp/

------------------------------------------------------------------------

WU Wien, Institute for Statistics and Mathematics

------------------------------------------------------------------------

Fr., 11.01.2019, 09:00, seminar room D4.4.008

WU Wien, 1020, Welthandelsplatz 1, WU Campus, building D4, 4th floor

Zach Feinstein (Washington University in St. Louis, US)

https://engineering.wustl.edu/Profiles/Pages/Zachary-Feinstein.aspx

"Pricing debt in an Eisenberg-Noe

interbank network with comonotonic endowments"

(Research seminar - Statistics and Mathematics)

For further details (including abstracts) see

https://www.wu.ac.at/en/statmath/research/resseminar/

To find the room on the WU Campus search for "D4.4.008" on:

http://gis.wu.ac.at/?roomShow=D4.4.008

------------------------------------------------------------------------

TU Wien, recruitment talks "Mathematische Stochastik"

------------------------------------------------------------------------

As already sent out before christmas holidays, the

recruitment talks for the full professorship in

robability Theory and Mathematical Statistics

("Universitätsprofessur für Mathematische Stochastik")

continue from today to this Wednesday.

For details, including abstract see:

https://fam.tuwien.ac.at/contact/temp/Berufungsvortraege_MSTOCH.pdf

------------------------------------------------------------------------

Dear colleagues,

the researchers

- Mathias Beiglböck and

- Nathanael Berestycki

from University of Vienna and

- Laszlo Erdös and

- Jan Maas

from IST Austria

start a new seminar:

Vienna Probability Seminar

^^^^^^^^^^^^^^^^^^^^^^^^^^

See:

https://mathematik.univie.ac.at/forschung/stochastik-und-finanzmathematik/v…

Talks of this seminar will usually not be posted on the FAM-news

mailinglist (unless talks are within the area of Financial and Actuarial

Mathematics).

In case you are interested in these talks you can subscribe yourself to

the corresponding mailinglist:

https://lists.univie.ac.at/mailman/listinfo/vps

Best wishes,

Sandra

--

Sandra Trenovatz <sandra(a)fam.tuwien.ac.at>

phone +43-1-58801-10511, mobile +43-664-5005638

Financial and Actuarial Mathematics (FAM), https://fam.tuwien.ac.at/

TU Wien, Wiedner Hauptstrasse 8/105-1, 1040 Vienna, Austria

(DVR: 0005886)

Dear friends of FAM & subscribers of FAM-news,

this week seems to be a quiet week for talks in the area of financial

and actuarial mathematics - nevertheless it will not be quiet at all.

The recruitment talks for the full professorship in Probability Theory

and Mathematical Statistics ("Universitätsprofessur für Mathematische

Stochastik") at TU Wien start this Tuesday. Stochastics/Probability

theory is important for many different fields of science and technology

- therefore we announce these talks.

As the next two weeks there will be (most probably) no talks I already

now wish you a Merry Christmas and a prosperous New Year 2019!

Sandra (Sandra Trenovatz, FAM, http://fam.tuwien.ac.at/)

---------------------------------------------------------------------

TU Wien, recruitment talks "Mathematische Stochastik"

---------------------------------------------------------------------

Tu., 18.12.2018, 10:30-12:30, lecture hall HS 17 Friedrich Hartmann

TU Wien, 1040, Karlsplatz 13, staircase 7, 3rd floor

Alexandre Stauffer (University of Bath)

https://sites.google.com/site/alexandrestauffer/

"Random aggregation processes: Long-time behavior,

phase transition and dendritic formation"

For details, including abstract see:

https://fam.tuwien.ac.at/contact/temp/Berufungsvortraege_MSTOCH.pdf

To find the lecture hall HS17 in the main building of TU Wien see:

https://fam.tuwien.ac.at/contact/temp/HS17.png

-----

Overview of all recruitment talks for the

full professorship in Probability Theory and Mathematical Statistics

("Universitätsprofessur für Mathematische Stochastik"):

Tu., 18.12.2018, HS 17:

10:30 Alexandre Stauffer

Mo., 07.01.2019, FH 3:

08:30 Omer Angel

10:30 Mykhaylo Shkolnikov

14:00 Erika Hausenblas

16:00 Johannes Muhle-Karbe

Tu., 08.01.2019, FH 2:

10:00 Nicolas Perkowski

13:30 Fabio Toninelli

16:00 Arnulf Jentzen

We., 09.01.2019, FH 3:

08:30 Noam Berger

10:30 Matthias Erbar

---------------------------------------------------------------------

{kind=link}